4 Special Accounting Considerations for Law Firms

Content

If you commingle your personal and business funds, you’re “piercing the veil,” and courts will ignore the legal protection that comes with incorporating. Plus, the more time and effort your accountant has to put into organizing your transactions, the more you pay them. When you have a trust account, you’re required to perform a three-way trust reconciliation every 30 to 90 days. We’ve seen firms using these accounts to hide assets or as a savings account. The reality is that there is no scenario where it’s okay to use your IOLTA in this way. They have their own rules and regulations that vary depending on your jurisdiction.

- Paragraph B enumerates minimal accounting controls for lawyer trust accounts.

- Only a small mistake or duplicated data entry may result in wasted time, mismatched records, billing complications, and even compliance violations.

- The advantage of this method is that it gives you a more realistic idea of income and expenses over a period of time.

- Use software like Uptime Practice to track billable hours, expenditures, and to keep your financial records in check.

- As a result, lawyers can automate a significant portion of their bookkeeping using accounting software.

With those items in place, we can tackle what to monitor and when. Finally, we’ll go over some common financial mistakes and how to avoid them. Once you have a strategy and budget in place, the work of day-to-day management sets in.

Three-way Reconciliation

Law firms are responsible for balances that do not match up, regardless of fault. You have tremendous duties and responsibilities as a lawyer and are scrutinized on many levels. As you know, the only way to avoid running afoul of laws and regulations is to have strong legal accounting and bookkeeping practices. Money leakage occurs when a firm struggles to send out invoices on time, track billable hours, and sending out late invoices. Leaking money happens when money that was supposed to be collected is not due to poor accounting practices. Well kept books for attorneys will aid accountants by giving them accurate financial data to work with.

Thankfully, there are a lot of tools available to help you manage your trust accounts, so you don’t have to go at it alone. Remember that your trust account is your client’s money, not yours. Here are five common law firm accounting obstacles and mistakes you should be aware of so you can avoid them. Accrual accounting gives you an idea of what income and expenses you have during a period of time, but doesn’t give a good picture of your actual cash flow. Keeping all of your business expenses in your business account makes it way easier for your accountant to sort through transactions come tax season. It’s not as dire as comingling your business and trust accounts, but it’s a slippery slope toward unorganized accounting. A fundamental concept in accounting and bookkeeping, double-entry accounting states that all financial transactions have equal and opposite effects in two different accounts.

Step 6: Streamline Time and Mileage Tracking

This is quite important, as you could be fined by the IRS for any errors. The fee structure for every https://www.bookstime.com/ment provider differs, and before you decide, ensure you know your numbers and the effect of the provider’s fee on your bottom line. As a result, it’s easy to make accounting a secondary priority thinking you can always deal with it later. Unfortunately, that attitude leads to some of the most frustrating accounting situations.

- Make sure your bookkeeping staff knows law firm accounting procedures.

- Budgeting makes it easier to set aside funds for larger expenses, such as annual bar association dues, legal research services, and information technology upgrades.

- Law firms are responsible for balances that do not match up, regardless of fault.

- A good bookkeeper can help you keep your finances accurate and up-to-date, which can help you attract clients and improve your image.

- With those distinctions in mind, it becomes easier to see which type of professional help you might need.

Regardless of your chosen method, remember that the IRS requires you to stick with just one to avoid tax compliance concerns. This GAAP-preferred accounting method helps law firms better visualize performance month to month for more effective firm budgeting and financial forecasting.

Law firm accounting vs. bookkeeping: What’s the difference?

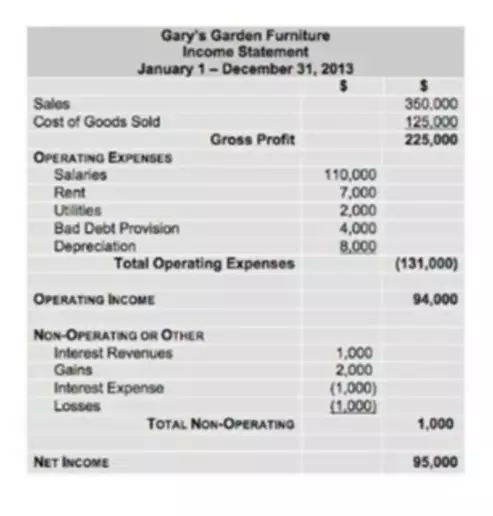

The income statement helps law firms decide if they can generate profit by decreasing costs, increasing revenues, or both. It also grades the efficiency of the strategies employed by the firm at the beginning of a financial period. Business owners and other executives can reference this statement or document to assess the success of their strategies. And depending on the outcome of their analysis, they can provide solutions to increase profit. Once again, it’s best to master the trust accounting rules well before you go into business for yourself. It’s one area you can’t afford to make mistakes because there’s rarely a chance to fix them later. Managing trust accounts is one of the unique aspects of legal accounting, and the consequences of mishandling them can be significant.

- Unfortunately, that often makes filing their first tax return a headache since they must go back and sort out what belongs where.

- You can do it manually or by using powerful accounting software to assist law firms in meeting this requirement.

- This number can be an average amount that takes into account that some months may be higher than others, depending on your area of practice and other market factors.

- Generally Accepted Accounting Principles are common accounting rules, standards, and procedures developed by theFinancial Accounting Standards Board .

- Essentially, double-entry accounting is an excellent safeguard against errors.

In this system, all law firm bookkeeping are categorized as one or the other. Personal InjuryTop 10 marketing strategies for Personal Injury lawyers.

Legal Accounting Software

It allows for more meaningful financial management that isn’t influenced by the ups and downs of cash flow. You’re much more likely to stay organized if you start off organized. By establishing—and following—best practices for accounting for law firms like the examples below, you’ll be better able to help your firm stay on track. IOLTA accounts are designed to keep client funds separate from your typical business or operating account—where you are allowed to accrue interest. Every law firm has a responsibility to stay compliant with ethics regulations, and your firm is no exception. Ethics rules vary in each jurisdiction, but there are some basic commonalities definitely some basics when it comes to accounting for law firms. The trust ledger is similar to a checkbook register and should include every trust transaction for every client.

Plus, no commitment or credit card is required, and you can cancel anytime. “The legal network for Baker Tilly will be in the US in the near future,” the firm’s chief executive officer, Alan Whitman, said in an interview. Withdrawals shall be made only by check payable to a named payee and not to cash, or by authorized bank transfer. Sasha serves as Managing Partner for Grow Law Firm, a Chicago-based digital marketing agency focused solely on specialized growth strategies for attorneys and their practices. It takes years to build a strong attorney reputation and one second to destroy it.